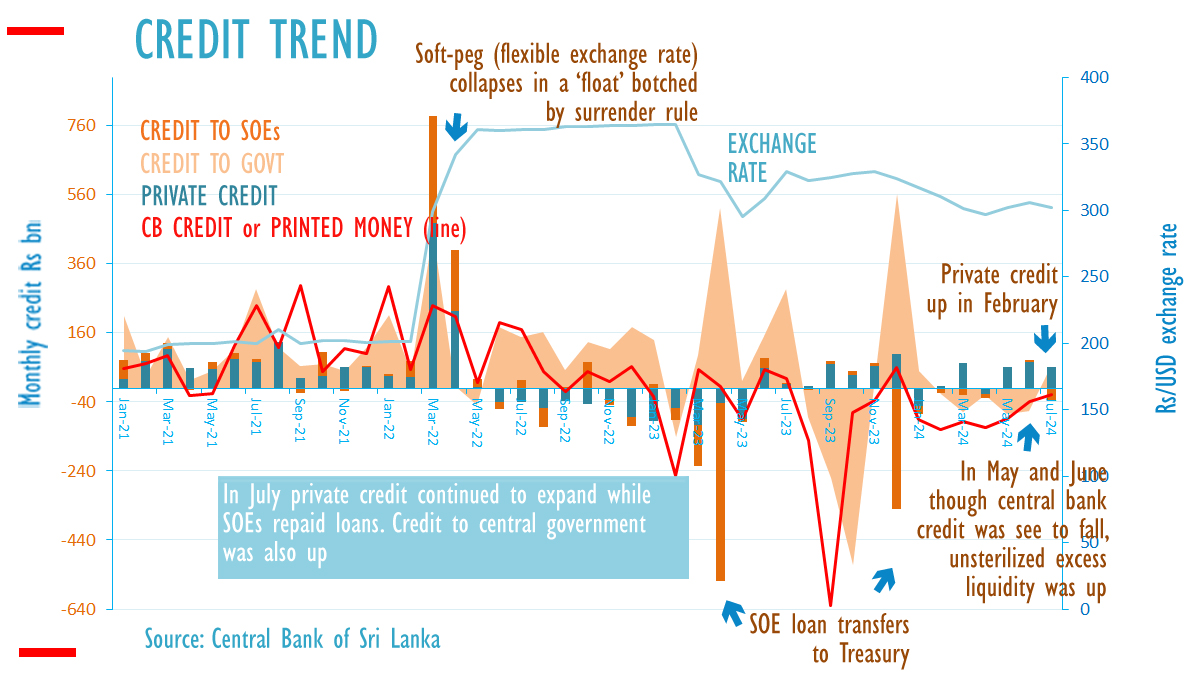

ECONOMYNEXT – Sri Lanka’s private credit expanded in 60 billion rupees in July 2024, on top of a 74 billion rise in June, official data show, while credit to state enterprises fell.

Banks loaned 82.7 billion rupees to the government in July (these include interest roll-overs which are effectively paper transactions) outside of central bank credit.

Central bank credit was a negative 19.8 billion rupees, making credit to government from the banking system as a whole 62.9 billion rupees.

In May and June 2024, central bank credit was shown as steeply negative based on the way data is reported, but large volumes of excess liquidity from dollar purchases remained unsterilized, putting pressure on the rupee as they were turned into credit.

Macroeconomists can pressure the currency by printing money to suppress the interbank call rate or allowing excess liquidity from dollar purchases to remain in the banking system and not intervening to redeem the rupees, when the hits the external sector through credit driven imports or other outflows.

Members of the public themselves cannot put pressure on the rupee, as they cannot print money, and in Sri Lanka the private sector is a net saver.

Savings of the public are turned into investment credit and imports through the banking system.

In Sri Lanka, especially after the end of a 30-year civil war balance of payments crises were created by targeting the average call money rate with inflationary open market operations as private credit picked up.

Inflationary open market operations or automatic unchecked lending through the standing liquidity (assured liquidity) encourage banks to engage in reckless lending without deposits, by borrowing from the central bank.

Because there are no counterparty limits, banks that re-finance credit with borrowings from the central bank, run large asset liability mis-matches.

The central bank, through inflationary outright purchase operations can clear these asset liability mis-matches and further drive credit without deposits, making credit and balance of payments deficits permanent.

The framework is based on a doctrine that it is possible for a reserve collecting central bank to target levels of inflation as high as 5 percent by printing money to cut rates.

Since inflationary open market operations are conducted against government securities, claims are made that the deficit is monetized, when OMO and standing facilities monetizes private bank credit using government securities bought in prior years.

Sri Lanka’s deficit lie: the inflationist narrative that leads to currency crises and default

Under the doctrine of flexible inflation targeting or printing money for growth (potential output), Sri Lanka therefore cannot avoid IMF programs, because the operating framework is deeply flawed.

Since September 2022, the central bank has run broadly deflationary policy, at an appropriate interest rate, helping keep the balance of payments in surplus.

State enterprises, particularly energy utilities have repaid debt with cost-based electricity and fuel sales, though kerosene is underpriced. (Colombo/Aug10/2024)