ADDRESSING BIODIVERSITY LOSS AND ECOSYSTEM DEGRADATION

Q: How are businesses addressing the challenges of biodiversity loss and ecosystem degradation?

A: As global climate responses accelerate, awareness of another challenge is also growing: nature and biodiversity loss. Biodiversity is defined by the UNEP as ‘the variety of life on Earth and the natural patterns it forms.’

As per the United Nations Environment Programme, it is essential to all processes that support life on Earth. People rely on natural ecosystems to ‘breathe fresh air, drink clean water, eat nutritious food and fight disease’ while businesses require ‘healthy people to work for them, and to buy their goods and services.’

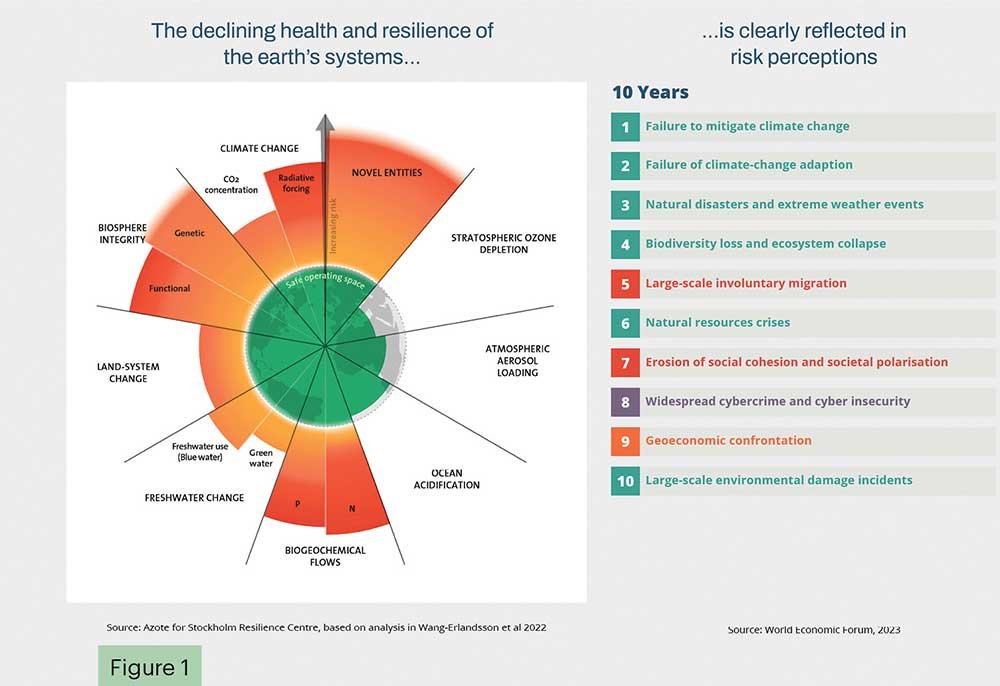

The global economy is already operating outside the safe zone for six of the nine planetary boundaries that are critical for maintaining the Earth’s stability.

And the World Economic Forum (WEF) Global Risks Report 2023 states that “biodiversity loss and ecosystem collapse” is one of the top five most severe global risks over the next decade.

The WEF report also outlines that climate change mitigation, food insecurity and biodiversity degradation are inextricably linked (refer Figure 1),

At the 2022 UN Biodiversity Conference of the Parties (COP15), a landmark agreement – the Kunming-Montreal Global Biodiversity Framework (GBF) – was adopted. The GBF provides direction for both public and private sectors to address biodiversity loss, restore ecosystems and protect indigenous rights, building upon existing regulatory and voluntary actions.

The roles of business and finance in addressing this challenge are cited in Target 15 of the GBF, which recommends legal and policy measures be taken to encourage businesses to regularly monitor, assess and disclose their risks, dependencies and impacts, reducing negative impacts on biodiversity and increasing positive ones.

In response to this historic agreement, an increase in the number of regional and country-based policies and regulations that outline new nature and biodiversity-related disclosures for businesses is anticipated – similar to how the Paris Agreement was a tipping point for action on climate change.

Q: How is the EU’s Corporate Sustainability Reporting Directive (CSRD) and its European Sustainability Reporting Standards (ESRS) playing a leading role in promoting nature-related disclosures?

A: In Europe, the CSRD mandates that businesses issue environmental, social and corporate governance (ESG) specific disclosures across numerous standards known as the ESRS including a standard that is specific to nature: ESRS E4 Biodiversity and Ecosystems.

Subject to materiality, the standard requires businesses to disclose topic specific policies, targets, action plans and resources, in relation to biodiversity and ecosystems, and recommends understanding biodiversity impacts and dependencies across the value chain.

Three environmental ESRSs have additional nature-related disclosures: E2 Pollution, E3 Water and Marine Resources, and E5 Resource Use and Circular Economy.

Q: What are the recommendations of the Taskforce on Nature-related Financial Disclosures (TNFD)?

A: TNFD developed a set of disclosure recommendations, which encourage and enable business and finance to assess, report and act on their nature-related dependencies, impacts, risks and opportunities. The recommendations will enable businesses and finance to integrate nature into decision making.

The TNFD disclosure recommendations are structured around four pillars, consistent with the Task Force on Climate-related Financial Disclosures (TCFD) and the International Sustainability Standards Board (ISSB).

They accommodate the different approaches to materiality in use currently, and are aligned with the goals and targets of the GBF.

Q: What other voluntary initiatives and frameworks are emerging in the corporate sector, to integrate nature and biodiversity disclosures into their reporting standards and practices?

A: There has also been an increase in the number of voluntary corporate reporting standards, guidance and frameworks developed and/or updated, to incorporate nature and biodiversity disclosures.

These include science-based targets for nature by the Science Based Targets Network (SBTN), Natural Capital Protocol principles and framework, and Global Reporting Initiative (GRI) standard 101: Biodiversity 2024.

The ISSB has also announced biodiversity, ecosystems and ecosystem services as being among their research agenda priorities for the next two years.

Q: How can stakeholders enhance their understanding of nature-related risks and opportunities, to effectively integrate them into strategies and financial decisions?

A: Despite the growing risks associated with accelerating nature loss, most businesses, investors and lenders today do not understand their dependencies and impacts on nature, and are inadequately accounting for nature-related risks and opportunities in their strategies and capital allocation decisions.

As the number of emerging nature-related regulations grows, and nature and biodiversity become increasingly important areas of focus, businesses should start preparing for and considering their responses to these nature-related disclosure requirements.

Telephone 5578634 | Email sampath.jayawardena@lk.ey.com | Website www.ey.com