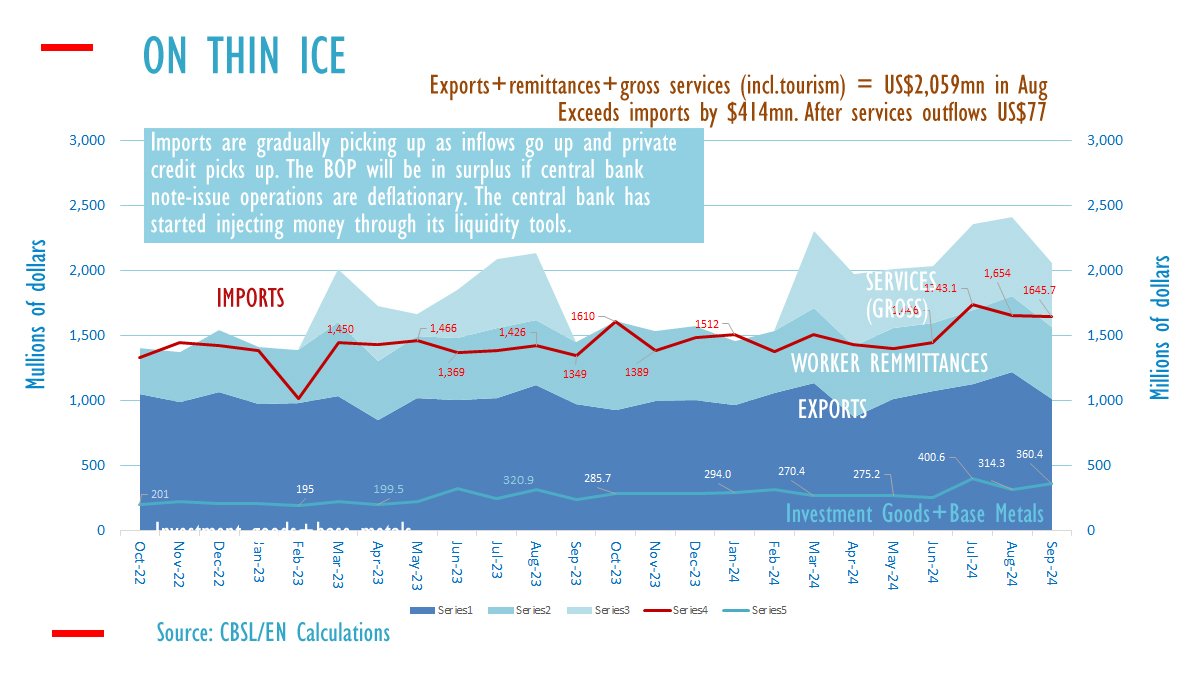

ECONOMYNEXT – Sri Lanka’s trade deficit widened to 634 million US dollars in September 2024 from 429 million dollars a month earlier, while the services surplus plunged to 156 million US dollars from 287 million US dollars in August, official data showed.

Imports remained at 1,645 million US dollars in September 2024, compared to 1,654 million US dollars in August while exports fell from 1,224 million US dollars to 1,011 million, and remittances were marginally down to 555.6 million US dollars, central bank data showed.

Gross services inflows including tourism also fell to 492 million US dollars, from 609 million dollars a month earlier, while services outflows increased to 336 million US dollars from 322 million dollars.

Gross inflows from exports, remittances, and services were 2,059 million dollars in September, exceeding imports by 414milion US dollars. After services outflows the gap fell to 77 million US dollars.

In September Sri Lanka’s private credit surged to 135 billion rupees (about 450 million US dollars) from about 60 billion rupees (200 million US dollars).

Since most private citizens and are savers, inflow are turned into outflows through the credit from the banking system (or withdrawals of cash balances).

Analysts have warned that Sri Lanka’s central bank has in the past printed money as private credit recovered, pumping the banking system full of excess liquidity to target mid corridor rate, triggering currency crises and frenzied foreign borrowings as private credit surge.

Sri Lanka’s central bank has started to aggressively inject print money through open market operations, to keep the short-term rates, which analysts warned will trigger external imbalances as private credit picks up.

Money is being printed close to its deposit facility rate of 8.25 percent and banks are being offered printed money through auctions for more than the daily bids in some days from around late August, data show.

Excess reserves in the banking system have started to climb indicating that not all of the printed money is being used as yet.

When the central bank prints money through its open market operations (taking in securities in bank balance sheets and turning them into money or circulating medium) bank can trade without deposits, financing imports or deposit withdrawals.

The central bank then imposes exchange controls, and import controls instead of correcting flaws in its inflationary operational framework.

The existence of exchange and import controls point a flawed operational framework based on post-1920 false doctrine taught in Anglophone universities in the West, analysts say. German speaking nations and successful East Asian exporters rejected the ideology.

The central bank has run deflationary policy since the second half of 2022 allowing the balance of payments to be in surplus. But early warnings have now been made that cracks are appearing the framework which will backfire once private credit picks up steadily.

Following the warning, an interesting debate has sprung up on the effects of printing money through open vs primary market purchases of domestic assets.

Analysts say instead of printing money to drive excess liquidity up, the central bank can cut the its floor policy rate and allow excess liquidity to build up only from dollar purchases (a surplus balance of payments)

In Lanka excess reserves appear to be excluded from the monetary base, which may be one of reason for the policy errors made by the central bank, and balance of payments crises, analysts say.

Sri Lanka’s private credit has not recovered fully as yet (for example credit may have been weaker in October), but there has been steady rise in investment goods and base metals imports indicating a pick up in investment.

Imports can also up for export manufacture. However packing credit for such imports could also be financed by open market operations and any deposit withdrawals by companies could also be similarly financed by new money preventing a correction in the credit system.

The balance of payments was still in surplus in September. (Colombo/Nov03/2024)